In our article titled “How Effective are AML Fines?†we explored the ineffectiveness of AML penalties, including the reasons that financial institutions are fined, the problem of recidivism of large banks, and how the inadequacy of such fines are due to a larger problem within the AML system. We also looked at how there are no metrics to determine the AML system’s success, and thus the effectiveness of AML fines.

What can lawmakers do to improve the AML system?

Critics have pointed out that AML regulations and guidelines tend to be vague and open to interpretation by the financial institutions and companies implementing them. This creates ambiguity in the application of rules, potentially allowing some entities to exploit loopholes or underestimate the importance of AML rules, leading to possible penalties.

Scenario-based guidance could also help financial institutions to better implement guidelines. These type of guidance documents outline different typologies of money laundering and how they might manifest in various industries or financial products. These real-world scenarios can serve as practical guides for compliance officers, making it easier to apply AML regulations in different contexts.

What can regulators do to improve the AML system?

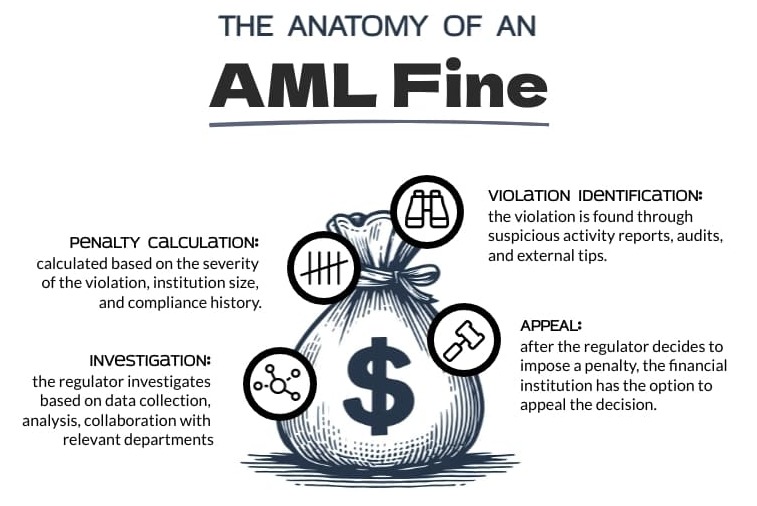

Penalties for non-compliance with AML rules are put forth by local regulators. These bodies often oversee investigations, conduct audits, and monitor financial institutions to ensure adherence to these regulations. They are also the go-to agencies for any issues, questions, or concerns related to anti-money laundering measures within their jurisdiction.

A tick-the-box approach can result in a weak compliance culture, turn AML into an administrative task instead of a pro-active one, and can result in overlooked suspicious activities and missed opportunities for detection, leading to AML penalties.

Regulators should redefine their role in the eyes of financial institutions and help them to steer away from a check-the-box mentality. This could be done by:

-

Outcome-based performance metrics: regulators should shift the focus from checklist-style compliance to outcome-based performance criterion. Financial institutions should be assessed based on the effectiveness of their AML programs and the actual reduction of money laundering risks, rather than just meeting procedural requirements. An example would be quantifying the actual number or value of money laundering incidents that were successfully identified, reported, and prevented.

Public-private collaboration platforms: regulators should create public-private collaboration platforms where they, law enforcement agencies, and financial institutions work together to share intelligence, knowledge, and approaches to AML. This collaborative approach can yield more effective strategies than mere compliance.

Incentive-based compliance: regulators could introduce incentive-based compliance models where financial institutions that proactively invest in AML technologies, training, and risk mitigation measures that shy away from tick-the-box processes are rewarded with regulatory benefits or reduced oversight.

Regulatory sandboxes: regulators could establish regulatory sandboxes where financial institutions can experiment with innovative AML solutions under controlled conditions. This allows for the testing and refinement of novel compliance approaches.

Stress testing for AML programs: regulators could set up a procedure to allow financial institutions to conduct stress tests on their AML programs, simulating various money laundering scenarios to assess their preparedness and effectiveness. This would allow financial institutions to see where and how their check-the-box strategies are not working.

What are alternatives to AML fines?

What we looked at in the above sections were ways in which lawmakers and regulators could help financial institutions fine-tune their AML programs and decrease their chances of receiving AML penalties, but are there alternatives or methods of improving AML fines?It is clear that AML fines don't help to improve the overall AML system, but they are still a necessary deterrent to financial misconduct and non-compliance. Below are some ideas to enhance their use:

TRANSPARENCY GUIDELINES - Provide to financial institutions clear and transparent guidelines for calculating fines. They should know how fines are determined, making the process less arbitrary and more predictable. This would allow financial institutions to have a good idea of what the monetary damage their shortcomings could cause.

PENALTY REINVESTMENT – Financial institutions could be asked to allocate a portion of their AML fine to be reinvested in improving the AML system itself. These funds can support research, technology upgrades, and training programs aimed at enhancing overall compliance efforts.

STRONGER ACCOUNTABILITY – Financial institutions should not be the only ones to be penalized but accountability should also be extended to compliance/AML officers and management. Individuals responsible for AML shortcomings should be fined or punished according to the severity of the deficiency. By holding compliance/AML officers and management accountable for their roles in addressing AML shortcomings, there will be a greater incentive for them to actively enforce and improve anti-money laundering measures.

UNINVESTABLE LIST – Financial institutions with AML shortcomings can be added to a list of “uninvestable†entities. This would extend their reputational damage beyond simple media coverage and would significantly impact their ability to attract investors, secure partnerships, and conduct business with other reputable entities. Being on an "uninvestable" list would serve as a powerful deterrent against AML deficiencies, as it would hurt the institution's credibility and trustworthiness in the eyes of potential stakeholders, thereby encouraging them to take AML compliance more seriously.

How could the efficiency of AML fines be assessed?

In part I of our article, it was noted how there are no metrics in place to evaluate the effectiveness of AML efforts across the globe, and hence there is little way to know if AML penalties are helping avert money laundering. Based on the available information, it appears that recidivism, the disproportionate size of fines relative to certain financial institutions' revenues, and the emphasis on penalizing non-compliance rather than effectively deterring money laundering all suggest that AML fines may not be effectively contributing to the fight against money laundering.Below are ways regulators could assess the success of AML fines:

-

Repeat offender identification: identify financial institutions that have previously faced AML fines and penalties. This requires maintaining a comprehensive record of AML enforcement actions and their outcomes.

Recidivism rates: calculate the recidivism rates among financial institutions. This involves determining how many institutions that have faced AML fines go on to commit further violations after the initial enforcement action.

Time lapses between offenses: measure the time intervals between AML enforcement actions against a specific institution. Shorter intervals may indicate that the fines and penalties were not effective in deterring future misconduct.

Impact on reputation: assess the reputational impact of AML fines on financial institutions. Evaluate whether being labelled a repeat offender negatively affects their business operations, customer trust, and market position.

Comparative analysis: compare the deterrence and recidivism rates across different jurisdictions or regions to identify best practices in deterring AML violations.

Public awareness and reporting: evaluate the role of public awareness campaigns and whistleblower programs in exposing and preventing repeat AML violations. Determine whether public engagement contributes to the detection of misconduct.

This data-driven approach can inform regulatory decisions and lead to adjustments in enforcement strategies to make them more effective in preventing money laundering.

A long road ahead…

While AML fines serve as a necessary tool for enforcement, there is a growing consensus that improvements are needed to make them more impactful and efficient. The goal is not merely to punish financial institutions for their shortcomings but to create a system that actively prevents and detects money laundering, thereby safeguarding the integrity of the financial system and protecting society from the grave consequences of illicit financial activities.