Do you like cookies? 🍪 We use cookies, just to track visits to our website, we store no personal details. By using our site, you acknowledge that you have read and understand our Cookie Policy, Privacy Policy, and our Terms of Service.

The Corporate sustainability reporting guideline (CSRD) is a new European regulation designed to enhance corporate transparency in terms of sustainable development. It replaces the Directive on the publication of non-financial and diversity-related information (NFRD). It considerably extends the scope of application and reporting requirements.

Aimed at harmonizing the format of extra-financial reports within the EU, this initiative marks a crucial step in the transition to a more sustainable and responsible economy.

CSRD or NFRD ?

The NFRD adopted in 2014, it marked a first step for the EU in requiring companies to disclose their sustainability performance. However, it was criticized for its limited scope and ambiguous reporting requirements. In this sense, the CSRD is an important development.

Unlike the NFRD, the CSRD applies not only to large public-interest companies, but also to large unlisted companies and listed SMEs. It requires companies to implement EU sustainability standards to ensure consistency and comparability of information, a requirement absent from the NFRD.

In addition, the CSRD introduces the concept of "double materiality". The NFRD requires companies to disclose not only the impact of sustainability issues on their financial performance, but also how their activities affect the environment and society. This more comprehensive and far-reaching approach represents a significant advance on the NFRD.

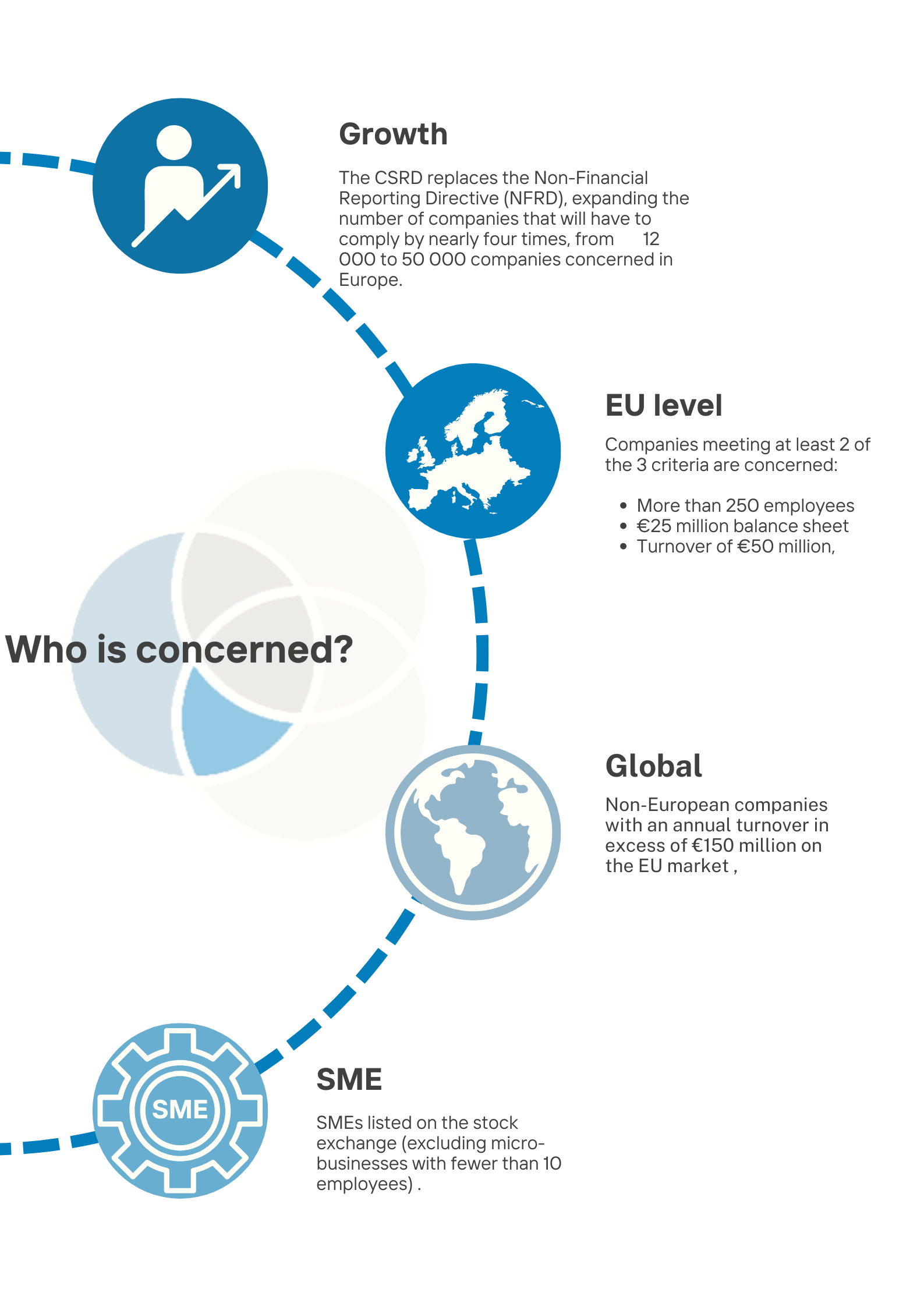

Who is affected by CSRD?

The CSRD applies to all large public-interest companies in the EU, including parent companies and subsidiaries, banks, insurance companies and other financial institutions. Unlike the NFRD, the CSRD also applies to large unlisted companies and listed SMEs.

Thus, the implementation of the CSRD will increase the number of companies involved by 194%, from 12,000 to 50,000 in Europe.

The determination criteria at European company level are based on the number of employees (over 250), balance sheet total (over EUR 25 million) and net sales (over EUR 50 million). Non-European companies with annual sales in excess of EUR 150 million on the European market will also be affected by the CSRD.

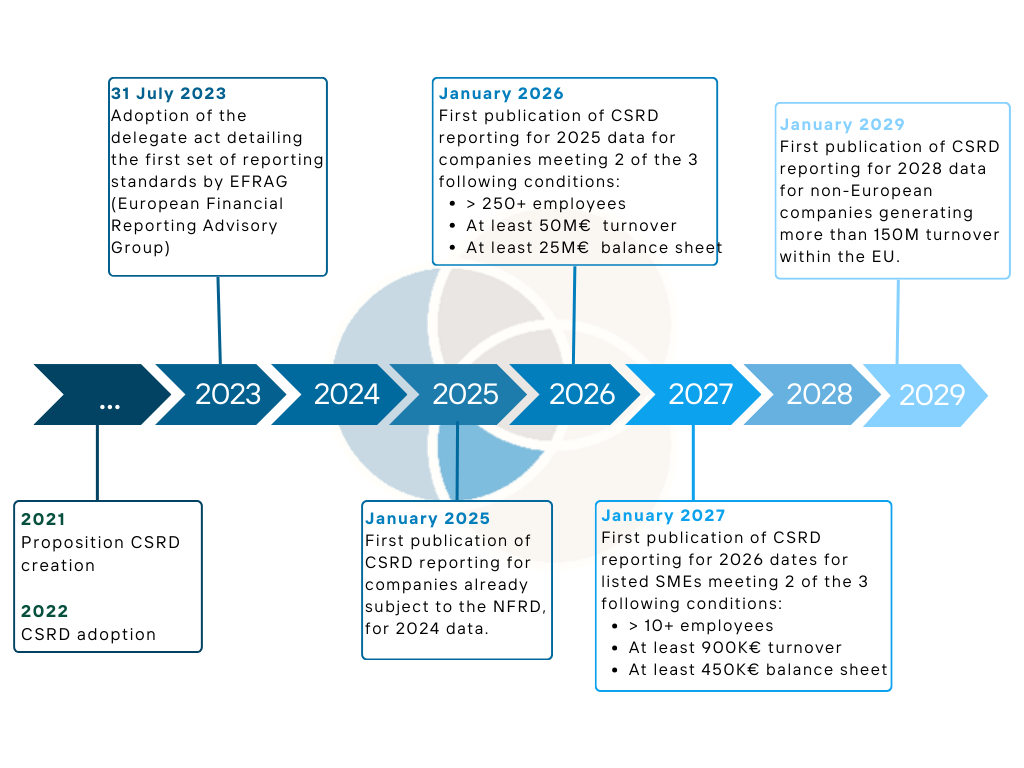

When does the CSRD apply?

The CSRD comes into force in 2024, with obligations of reporting from 2025.

Each category of company meeting the above criteria will therefore have to comply with the European directive according to a different timetable:

What deliverables are expected?

The companies concerned will have to publish a comprehensive annual sustainability report, including detailed information on :

1

Sustainability strategy : A description of how the company integrates sustainability into its activities and overall strategy.

2

Sustainability policies : Specific policies and procedures in place to manage environmental, social and governance issues (ESG ).

3

Sustainability risks: Identification of ESG risks facing the company and plans to mitigate them.

4

Sustainability performance : Measures and key performance indicators (KPIs) to track the company's progress in sustainability.

This report must cover a wide range of areas, including ESG :

Subject

Definitions

Environmental

Greenhouse gas emissions, resource use, pollution, climate change, waste and water management.

Social

Working conditions, human rights, diversity, inclusion, health and safety.

Governance

Governance structure, ethics, anti-corruption.

Economie

Impact on the local economy and community.

What are EU sustainability standards?

To ensure consistency and comparability of information, companies must use the following EU sustainability standards "ESRS" developed by the European Financial Reporting Advisory Group (EFRAG).

These standards will cover specific areas such as :

1

Greenhouse gas emissions

2

Biodiversity

3

Water and waste

4

Working conditions

5

Respect for human rights

Sustainability reports must be audited by an independent external auditor to guarantee their reliability and accuracy.

IMPLICATIONS

The EU's new sustainability declaration requirements will therefore have a significant impact on the companies concerned.

They will have to :

Set up robust systems for collecting and managing sustainability data.

Develop clear and comprehensive sustainability strategies and policies.

Implement measures to measure and monitor their sustainability performance.

Engaging stakeholders on their sustainability issues.

BENEFITS

Despite the challenges involved in its implementation, the new requirements also present a number of potential benefits for companies, such as :

Improving transparency and accountability

Strengthening investor and customer confidence

Better identification and management of ESG risks

Better strategic decision-making

Contributing to long-term sustainability.

What are the other key points of the CSRD?

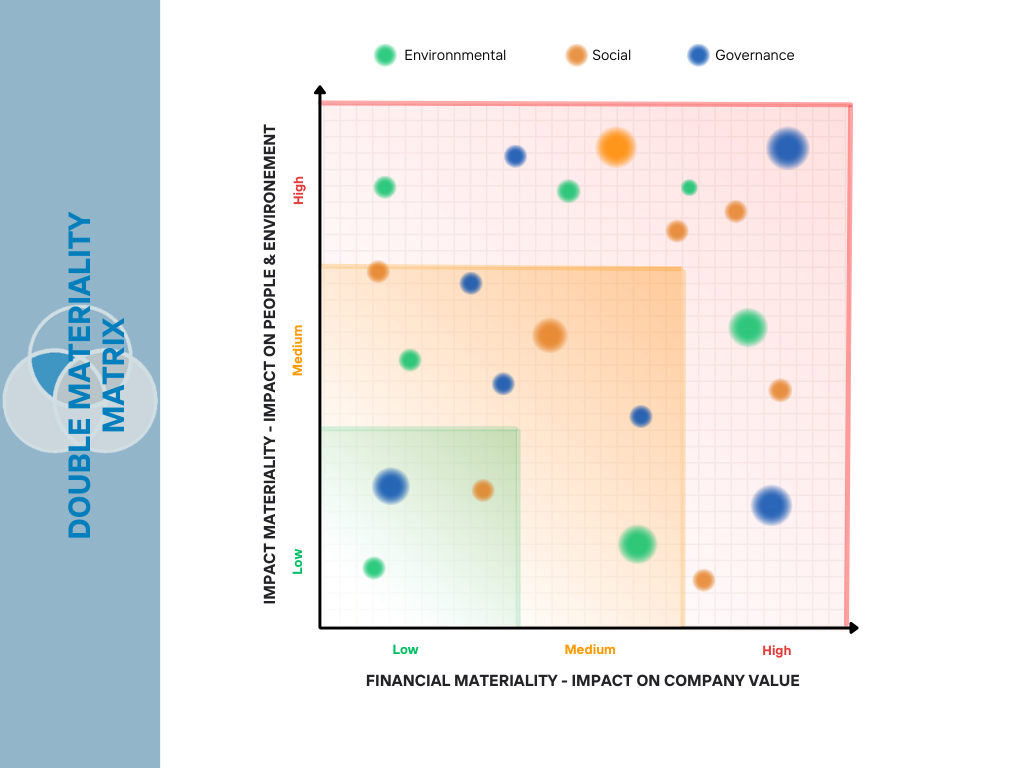

CSRD also introduces an entirely new concept: the "double materiality".

This means that companies must not only disclose how sustainability issues affect their financial performance (financial materiality), but also how their activities affect the environment and society (extra-financial materiality).

In addition, the CSRD strengthens the role of directors in overseeing the company's sustainability strategy. Directors will be held accountable for how they integrate sustainability issues into their business strategy and decision-making processes.

The CSRD also provides for penalties for companies that fail to comply with reporting requirements. These sanctions will be determined by the Member States, but they must be effective, proportionate and dissuasive.

Finally, the CSRD provides for the creation of a european sustainability reporting platform. The aim of this platform is to facilitate public access to corporate sustainability information and help improve the quality and comparability of sustainability reports.

CSRD in a nutshell

The CSRD is a significant change compared to the NFRD by strengthening reporting requirements sustainability standards for European companies. By extending the scope of application and introducing new concepts such as double materiality, the CSRD aims to promote greater transparency and corporate responsibility in terms of sustainability.

The companies concerned must publish an annual sustainability report , which will include detailed information on their sustainability strategy, policies, risks and performance. EU sustainability standards and external verification of sustainability reports will enhance consistency, comparability and reliability of information.

The CSRD comes into force in 2024. Companies will therefore need to start collecting and tracking relevant data in order to comply with the new requirements, according to a precise timetable depending on the nature and size of their business.

In short, CSRD represents a key step in the transition to a more sustainable and responsible economy in Europe. By strengthening transparency and corporate responsibility in terms of sustainability, CSRD will help to improve decision-making by investors, consumers and other stakeholders.

Are financial sanctions and embargoes effective in deterring rogue states? Learn the history of sanctions, the pros and ...

EuropeTue 28 February 2023

Experts in risk management and regulatory compliance

Pideeco is a consultancy firm providing legal services, business solutions, operational assistance and educational material for professionals in the financial industry.

We are based in Brussels and we specialize in regulatory risk compliance services covering the Eurozone.

Pideeco combines professional Regulatory knowledge and technical expertise to safeguard your business’ reputational and operational risk. Our unique customer-centric approach helps us build strategical and legitimate cost-efficient remedies.

Working with us means reaching out to complementary people, allowing for original thinking and innovative vision.