The exponential growth of technology is leading to the disruption of numerous sectors including telecommunications, robotics, science, and finance. As banks are slowly adapting to high-tech innovations, the world of compliance and AML will face unprecedented changes and challenges in the near future.

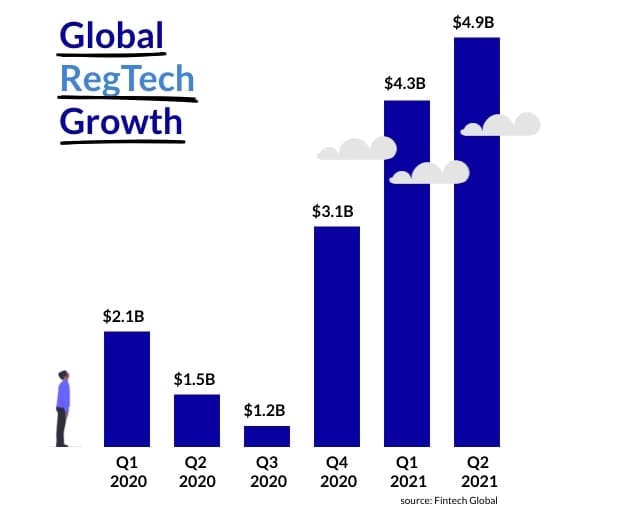

The world of banking is at the dawn of a technological renaissance that will forever change our perception of finance and money. Novelties such as the FinTech and RegTech sectors are already exploiting artificial intelligence (AI), robotic process automation (RPA), and blockchain technology for banking services. Analysts estimate a compound annual growth rate of 26.87% for the global FinTech market and 20.3% for the global RegTech market up until 2025, according to Yahoo! Finance.

Technologies such as AI, Internet of Things, invisible banking, and quantum computing are predicted to supplant the classic banking system soon, ushering an era of automation, tailored products, and risk-averting predictive models.

But if transaction monitoring systems can be automated to analyse transactions better than a human, suspicious client activity can be detected by a computer in mere seconds, STRs can be written by an AI, and quantum computers can predict customer behaviour, what will the future hold for AML and compliance professionals?

What is the future of AML with AI and machine learning?

The world of artificial intelligence is one of the fastest growing technological sectors in the world. It is forecasted that in 2021 AI augmentation in companies will earn $2.9 trillion in business value and free 6.2 billion hours of worker productivity. The global AI market is also expected to hit $89.8 billion by 2025 according to Aumcore.

FinTech and RegTech firms are beginning to release AML solutions for banks that use artificial intelligence and machine learning to analyse transaction data, discover adverse media on clients, and vastly improve and simplify customer due diligence processes.

Not-so-distant future AI and machine learning solutions will be capable of rating the risk of suspicious behaviour of clients, identify relationships amongst suspicious individuals and entities, detect changes in customer behaviour, and conduct lookbacks in mere hours. This will eliminate the need to use manual labour for such tasks.

A 2018 report by the World Economic Forum titled “The New Physics of Financial Services†demonstrated that AI automation, both in customer service and administration, will radically transform how banks operate.

The risk is that these solutions will remove the need for data analysis roles such as AML analysts, transaction monitoring analysts, and possibly KYC analysts. However, AI will not spell the death of compliance positions. AML professionals will still be needed to run the software, communicate with the coders to tweak the systems, and lend their expertise in detecting new money laundering techniques. This may even create a whole new field of artistry in which AML professionals will become coders, developers, and project managers dedicated to AI solutions for financial institutions.

How will Internet of Things shape the future of AML?

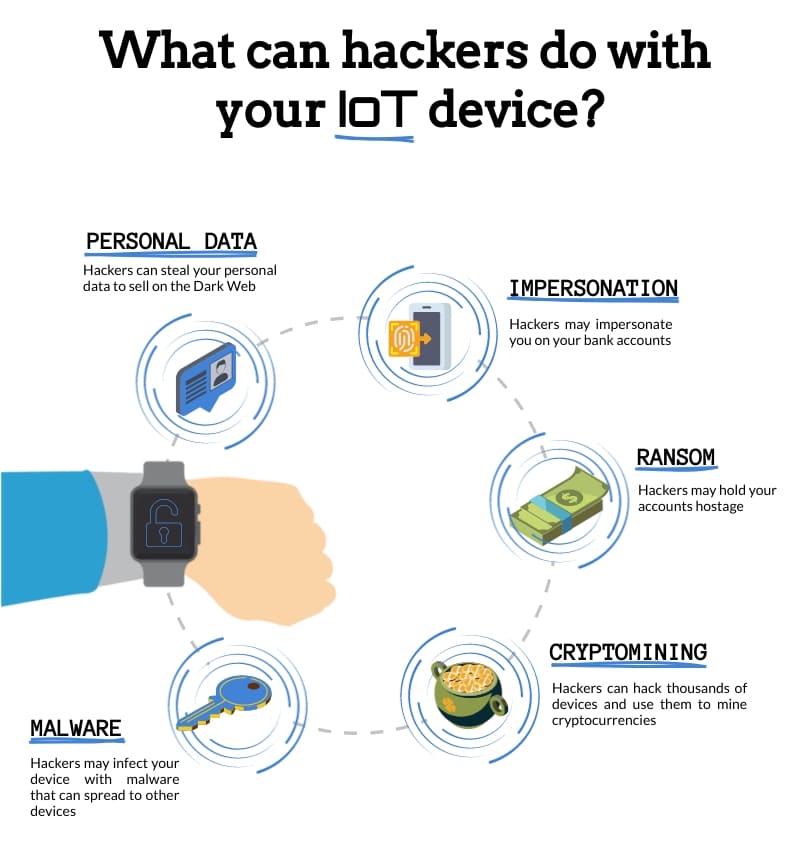

Internet of Things (IoT) is currently a hot topic in the world of finance and banking. It is a network of physical objects – smartphones, tablets, smartwatches, smart rings, other wearables, etc. – connected to exchange data with each other over the internet. We are already seeing this today with smartphones linked to our bank accounts that are used to pay bills in restaurants and shops.

The IoT market is expected to grow at a compound annual growth rate of 52.1% until 2024 and is estimated to be worth $2 billion by 2023 according to ReportsnReports. Forecasts predict that connected devices through IoT will amount to 75.44 billion globally by 2025 and that everyday payment objects such as credit and debit cards will become obsolete.

Coupled with AI, IoT will become a powerful tool for KYC. Interconnected devices such as smartphones, smart eye wear, and tablets can create a customer’s digital persona offering a vast amount of information on the person’s identity and financial behaviour. KYC processes can be accelerated and even be completed in real time using the person’s downloaded data while AI can perform financial pattern recognition and identify high-risk customers.

However, IoT poses numerous security risks. Spyware, password theft, and device imitation can spread to thousands of devices through one security hole and infect entire networks. Confidential information such as facial recognition, data or audio, and video recordings can be used to conduct fraudulent activities on a person’s bank account. Stolen data has great value on illicit markets found on the Dark Web where account information and identity documents are sold.

IoT will lessen the need for KYC and screening analysts while increase the demand for cybersecurity specialists. KYC professionals will still be needed to run the software, offer advice on new methods of identify fraud, and give a second opinion on specific cases. They will likely work alongside cybersecurity experts with deep knowledge of digital hijacking methods for money laundering and identity theft/impersonation.

How will invisible banking influence the sphere of AML?

Closely connected to IoT and artificial intelligence is the notion of invisible banking. Blending the two together, along with voice banking, blockchain technology, and FinTech technology, invisible banking aims at integrating financial services into our lives without us really noticing. Individuals will be able to pay for parking with a device connected to their car that automatically extracts the amount needed from their bank account. They will also be able to pay for their bus ticket just by stepping inside the bus without the need to physically purchase the ticket. Invisible banking aspires at make banking become part of a person’s subconscious.

The removal of physical banks and the converging of their services towards electronic devices may pose numerous risks. Criminals will be able to carry out smurfing and structuring schemes more easily toward front businesses, pumping them with ill-gotten gains through small transactions just by walking inside of them. A complicated web of small payments through connected businesses can conceal the origin of criminal funds making them harder to trace.

Fraudsters may also hack or steal devices to use for their own needs while hackers can bring down, manipulate, or steal information and money through cyberattacks.

Positions in fraud such as fraud examiners and specialists will gain ground in financial institutions, either working alongside AML professionals or fusing with their roles. AML experts will be needed to detect new laundering techniques and thus update the AI software to capture new suspicious behaviour. They will also be needed to integrate new regulations and laws into the system. Cybersecurity will become a fundamental aspect of invisible banking as well, creating more positions within that domain.

How will quantum computing shape the future of AML?

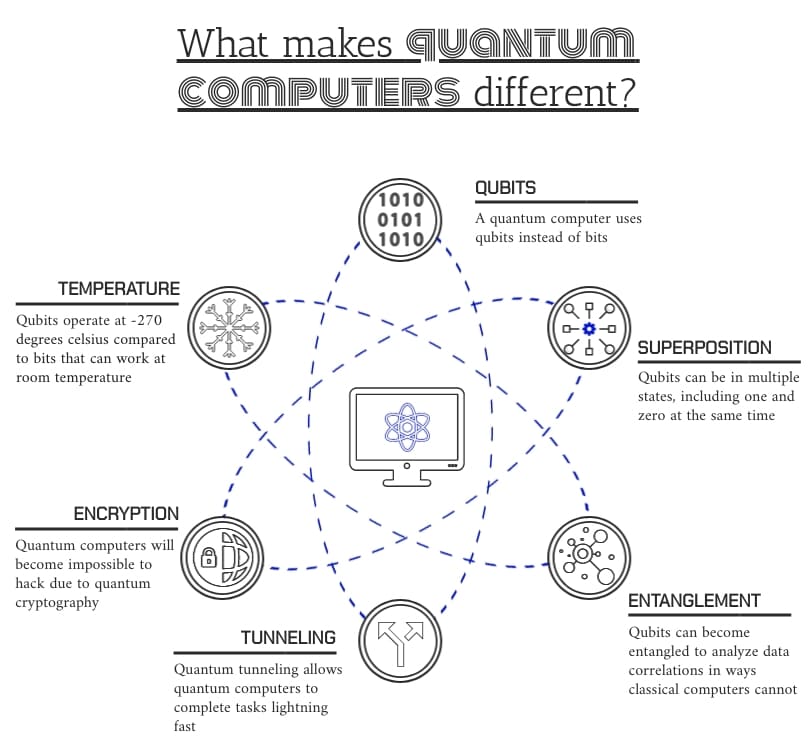

Quantum computers are set to revolutionize the world of computing. Using quantum mechanics, or the physics and interaction of subatomic particles (photons, electrons, etc.), the computational power of a single computer will increase in unimaginable ways.The global quantum computing sector is expected to have a compound annual growth rate of 30% until 2027 with a projected $667.3 million market size by that year according to Research Dive. Financial institutions such as BBVA, ABN Amro, CaixaBank, and Standard Chartered Bank are already researching and studying the benefits of quantum computing in the world of banking.

These benefits include the analysis of gargantuan unstructured data, the improvement of customer service by offering timelier and more relevant offers, the calculation of customer credit risk, and equity trading optimization. Quantum computer will also be able to create models to classify and take onboarding decisions for KYC processes and may also predict customer behaviour. Coupled with AI, its capabilities may be endless.

While it is hard to predict if such computers may supplant certain functions within the compliance domain, it is most likely that all AML and compliance professionals will need to become accustomed to the complexities of quantum technology in the future. The fusion of AI and quantum computers may spell the doom of AML analysts and other similar roles, but AML professionals will always be needed to help tweak the detection software, analyse and fine-tune its detection rules, improve its functionnalities, and advise on new detection and money laundering methodologies. It is possible that AML professionals may either become software architects or software runners.

Commercialization of quantum computers is predicted to happen in five years’ time.

What does the future hold for AML officers?

What we have seen from this brief analysis on artificial intelligence & machine learning, Internet of Things, invisible banking, and quantum computing is that automation will reign supreme in the future of banking. Manual analysis jobs, including AML and KYC analysts, will most likely be replaced by AIs that can do faster and more precise work.

As the world of financial institutions will become more technological, there will probably be a shift for AML professionals from the world of banking to the worlds of FinTech and RegTech. AML specialists will need to acquire a certain degree of technical proficiency with coding and software development as the spotlight on anti-money laundering will focus on creating powerful and intelligent tools to counter the flow of dark money.

These incredible technological advances will not doom the sphere of AML to antiquity. We can’t predict what new positions and jobs will be created out these future advances or what incredible technologies may arise in the coming years. Who would have known 20 years ago that any of the technological wonders listed above would exist today?

The best way for AML professionals to not be overwhelmed by these novelties is to constantly update their knowledge on upcoming technologies. The more one understands what the future holds for their job, the more one can adapt and evolve in the approaching disruptive financial landscape. Ignoring future technologies may lead to getting left behind and finding their line of work obsolete.

As long as crime exists, anti-financial crimes roles will still be needed in one form or another.

AMLComplianceDarkwebData breachDue DiligenceDigitalData SecurityFinancial InstitutionsKnow your CustomerMoney LaunderingRegTechFinTechRisk

This article has proven to be very helpful to me. Articles as such might be much helpful to you to enhance your knowledge base. You shall learn a lot from this. They provides valuable information such as IT Consulting Services, Telecommunication, Graduate Recruitment, Executive Appointment, Digital Marketing, Sales and Marketing

This is mind blowing, thanks for sharing this valuable content.