Do you like cookies? 🍪 We use cookies, just to track visits to our website, we store no personal details. By using our site, you acknowledge that you have read and understand our Cookie Policy, Privacy Policy, and our Terms of Service.

With the convenience of online shopping and the ability to purchase goods and services from anywhere in the world, e-commerce has revolutionized the way we do business. The COVID-19 pandemic has only accelerated this trend, forcing many businesses to shift their operations online to stay afloat. But with the rapid growth of e-commerce comes new challenges, including security concerns, privacy issues, and regulatory compliance.

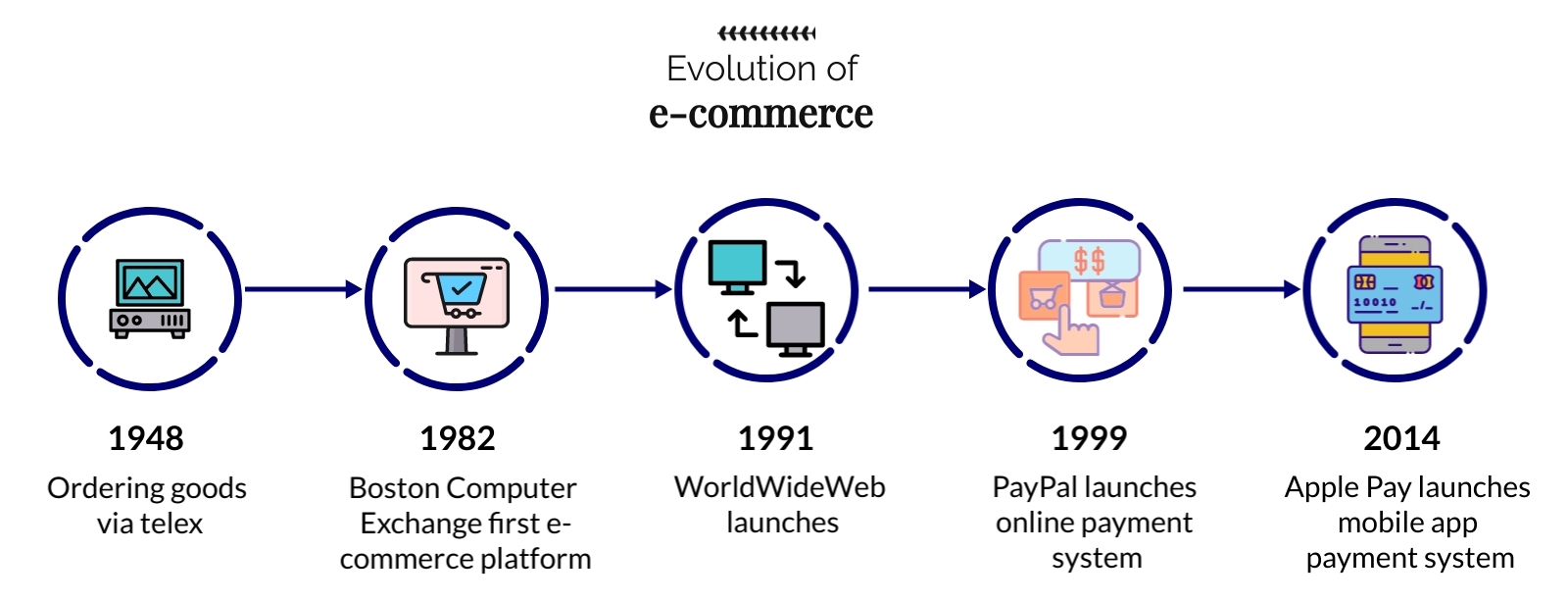

E-commerce, short for electronic commerce, refers to the exchange of all types of goods, services, funds, or data over an electronic network, usually the internet. This type of business transaction can take place between businesses (B2B), businesses to consumers (B2C) and consumers to other consumers (C2C).

E-commerce typically involves a three-step process that begins with accepting the customer's order. The second step is processing the payment, which involves securely processing the customer's payment through a payment gateway. The final step is to ship the order promptly. This is a crucial step in maintaining customer satisfaction and loyalty.

The e-commerce market is forecasted to achieve a revenue of US$4.00 trillion in 2023, and it is anticipated to experience a compound annual growth rate of 11.34% between 2023 and 2027, leading to an estimated market size of US$6.15 trillion by 2027.

In this article, we will explore the world of e-commerce, examining its benefits and drawbacks, and providing insights into how businesses and consumers can navigate this complex landscape.

What are the advantages and disadvantages of e-commerce?

There are many advantages to conducting business on an online platform . Understanding how e-commerce works can help individuals and businesses leverage these benefits to their advantage. Some of the benefits that E-commerce offers are a large market with a lower cost to start your business. You also have the possibility to respond quickly to any new trends. E-commerce is not limited to physical space.

Although e-commerce provides many benefits for businesses, it also comes with its own set of challenges. These challenges include the absence of the personal touch and physical interaction with sales advisors that is present in stores. In addition, the lack of tactile touch can make some customers nervous about what to expect from their purchases.

E-commerce businesses and customers must also be vigilant about credit card fraud and IT security issues. If an online business operates across multiple territories and sells to customers in different regions, it must comply with the laws and regulations in each jurisdiction. This can create a host of complexities in areas such as compliance.

What are crimes related to e-commerce?

E-commerce has revolutionized the way we shop and do business, making it easier and more convenient for consumers and companies to connect and transact. However, as with any technology-driven platform, e-commerce has also created new opportunities for criminal activity. Cybercriminals have found ways to exploit vulnerabilities in online transactions and leverage the anonymity and global reach of the internet to perpetrate a wide range of crimes, from (tax)fraud to money laundering.

Transaction laundering is a type of electronic money laundering that enables illicit merchants to hide their transactions by processing sales through the payment credentials of a legitimate vendor. This fraudulent practice allows illegal businesses to bypass security measures and carry out financial activities that would otherwise be prohibited. By exploiting legitimate payment channels, transaction launderers can evade detection and continue to engage in criminal activities, which can have serious consequences for businesses, consumers, and the financial system.

The rapid expansion of e-commerce and mobile payments has given rise to a surge in transaction laundering. It is estimated that between 2023 and 2027, online payment fraud will cause global merchant losses that will surpass $343 billion in total. This underscores the urgent need for robust measures to combat this type of financial crime and protect the integrity of the financial system.

E-commerce has given rise to a variety of frauds that can have a significant impact on both consumers and businesses. Refund fraud is a common tactic used by fraudsters who are unable to receive goods or cash out using stolen credit cards. Another type of fraud is interception, where the fraudster places an order using a valid billing and shipping address, but then attempts to intercept the goods for themselves.

These and other types of e-commerce fraud underscore the importance of vigilance and caution when engaging in online transactions. E-commerce is also being used as a tool for tax evasion. Several factors have led to e-commerce being recognized as a means for tax evasion. Among these factors is the challenge faced by tax authorities in tracking and monitoring e-commerce transactions, particularly those involving cross-border sales.

What is the compliance legislation related to e-commerce?

In the USA, the Bank Secrecy Act (BSA) requires U.S. financial institutions to assist U.S. government agencies to detect and prevent money laundering. Under the BSA, e-commerce platforms that meet certain criteria are considered "money services businesses" (MSBs) and are subject to AML program requirements.

An MSB is defined as any person or business that provides certain financial services, including money transmission, check cashing, and currency exchange. E-commerce platforms that allow customers to make payments, transfer funds, or exchange currencies may fall under the definition of an MSB and be subject to AML program requirements.

In the European Union , the DAC 7 directive (effective from 1 January 2023) aims to increase tax transparency in the digital sector. This is achieved by obliging reporting platform operators to collect and report specific information on sellers using their platforms for certain commercial activities.

In addition, EU member states are required to automatically exchange this information. The rules set out in the Fifth Anti-Money Laundering Directive (AMLD5) also apply to e-commerce businesses under the umbrella of obliged entities. Online businesses are now required to follow KYC procedures and EDD procedures.

Internationally, there is the the Payment Card Industry Data Security Standard (PCI DSS). This standard applies to any business that accepts credit card payments. It outlines the security requirements for the processing, storage, and transmission of credit card information. The PCI DSS was created by American Express, Discover Financial Services, JCB International, Mastercard, and Visa in December 2004.

PCI DSS has been updated on 22 March 2022. The objective of the update is to address the changing security requirements of the payment industry, emphasize the importance of ongoing security measures, provide greater flexibility, and enhance procedures for organizations utilizing diverse methods to attain their security objectives.

What are red flags related to e-commerce?

In the world of e-commerce, there are red flags that may help you become aware of any criminal activity on an online platform. The list of red flags needs to be updated as criminals are becoming more creative and smarter.

As a merchant, you have to be aware of the following red flags concerning your customers:

1

Address inconsistencies

2

Rush or overnight shipping

3

Fake or suspicious contact information

As a customer, the following red flags should raise questions:

1

Prices are very low

2

You spot spelling errors in the URL

3

New website without much information

As an AML analyst, you have to be aware of the following red flags:

1

Customers or merchants residing in countries who don’t take high regard of AML regulations

2

Individuals involved in economic or commercial endeavors or industries that are considered vulnerable to money laundering

3

Account transactions or other actions that do not align with the information and records gathered through due diligence

What is the future of e-commerce compliance?

The future of legal regulations concerning e-commerce is likely to involve increased attention and scrutiny of lawmakers and regulatory bodies. As e-commerce continues to grow and play an increasingly significant role in the global economy, there is a growing recognition that the legal framework governing online transactions needs to be updated and expanded.

The Digital Service Act Package (starting on January 1st, 2024) will enforce a fresh set of regulations for online intermediary services. These new rules aim to dictate how these services and their procedures should be designed. The regulations include additional responsibilities to curb the spread of illicit content and illegal products on the internet, improve the protection of minors, and provide users with greater options and improved information. The duties of various online entities will be correpsondant with their role, size, and impact on the online ecosystem.

One area of focus is likely to be data privacy and security, as concerns about online security and the protection of personal information continue to mount. E-commerce businesses will need to be diligent in their efforts to protect customer data and ensure compliance with emerging data privacy laws and regulations.

Another area of focus is likely to be international trade and taxation as e-commerce blurs the lines between national boundaries and makes it easier for businesses to operate across borders. As a result, there will be a growing need for legal frameworks that can effectively regulate cross-border transactions and prevent abuses of the system.

This article explains well how AML compliance is becoming essential in e-commerce. Building trust with secure transactions and proper checks like KYC helps prevent fraud.

What are the main EU directives related to money laundering and terrorist financing? This article explains the character...

ComplianceWed 15 March 2023

Experts in risk management and regulatory compliance

Pideeco is a consultancy firm providing legal services, business solutions, operational assistance and educational material for professionals in the financial industry.

We are based in Brussels and we specialize in regulatory risk compliance services covering the Eurozone.

Pideeco combines professional Regulatory knowledge and technical expertise to safeguard your business’ reputational and operational risk. Our unique customer-centric approach helps us build strategical and legitimate cost-efficient remedies.

Working with us means reaching out to complementary people, allowing for original thinking and innovative vision.

This article explains well how AML compliance is becoming essential in e-commerce. Building trust with secure transactions and proper checks like KYC helps prevent fraud.