Do you like cookies? 🍪 We use cookies, just to track visits to our website, we store no personal details. By using our site, you acknowledge that you have read and understand our Cookie Policy, Privacy Policy, and our Terms of Service.

The recent creation of Benchmark Regulation has been the catalyst for a major transition from the old regime of benchmarks towards new and alternative reference rates set to transform the world of finance.

In the past years, a global benchmark reform process has been creating a shift from the old interbank offered rates (IBORs) towards novel, robust, and transparent overnight risk-free rates (RFRs). This will lead to the discontinuation of several historically important benchmarks in Europe that have dominated the landscape of mortgages and complex financial transactions for decades.

The shift is rooted in the LIBOR scandal of 2012 which prompted the International Organization of Securities Commissions (IOSCO) to create a set of principles in 2013 for issues pertaining to benchmarks.

These were later incorporated into EU legislation, thus setting up what is known as Benchmark Regulation (BMR).

What is a benchmark and why are they important?

An interest rate benchmark, also known as a reference rate, is a publicly accessible rate used for mortgages, bank overdrafts, and other more complex financial investments.

Banks have excess reserves of money and instead of letting them sit idly, they loan them to one another with an interest rate for periods of time raging from one day, one month, six months, etc. all the way up to twelve months. This is known as interbank lending.

For each different benchmark, a panel of banks will input every morning their rates for each maturity. The calculation of the average, which determines the reference rate, is done by an independent body such as a benchmark administrator.

These rates have a paramount influence outside the interbank lending market. If the rate at which a bank can borrow money from another bank can increase or decrease, so will the bank’s tendency to increase/decrease the rates it offers to its clients, both the rates at which it borrows from private individuals and the rates at which it lends to companies and households. The rates are also used for the issuance of securities with variable rates, options, forward contracts and swaps.

One of the most influential benchmarks is the London Interbank Offered Rate (LIBOR) used for short-term interest rates around the world and is calculated for five currencies. In mid-2018, roughly $400 trillion worth of financial contracts were referenced to the LIBOR. Other major benchmarks include TIBOR (Japan) and HIBOR (Hong Kong). In Europe the two major ones are Euribor (Euro Interbank Offer Rate) and Eonia (Euro Overnight Index Average).

How is BMR creating a shift towards new benchmarks?

The 2012 Libor scandal, in which banks were manipulating interest rates for their benefit, led to the creation of a set of principles for the conduct of benchmark administrators.

The IOSCO Principles for Financial Benchmarks of 2013 touch upon the following guidelines: the responsibility of the Administrator, conflicts of interest, internal oversight, the quality of the benchmark, and accountability. The principles were implemented in the Regulation (EU) 2016/1011 of the European Parliament and of the Council of 8 June 2016 which came into effect in 2018.

Overall Responsibility of the Administrator

Oversight of third parties

Conflicts of interest for Administrators

Control framework for Administrators

Internal oversight

Quality of the benchmark

Accountability

IOSCO Principles

The result was a scramble by benchmark administrators to comply to the new rules.

Starting from the 1st of January 2018, existing benchmark administrators had a two-year period to apply for authorisation or registration with their competent authority. They also needed to produce and maintain sturdy written plans to cover any material changes or the discontinuance of their benchmarks. The contracts with their clients also needed to reflect the changes in these plans.

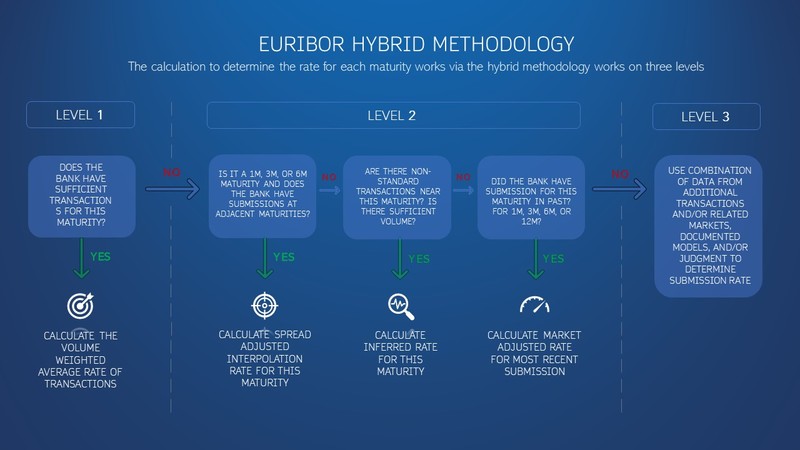

These changes led to the reforming of Euribor, particularly the calculation of its rate.

Its original methodology was morphed into a “hybrid methodologyâ€, meaning that the contributions of its panel banks will consist of transactions from a range of markets closely related to the unsecured euro money market compared to the old methodology of having the banks input their preferred rates. The new Euribor came into effect at the end of 2019.

Other benchmarks cannot comply to BMR and must be discontinued. One of these is Eonia, which has been a fundamental European benchmark for overnight unsecured lending transactions since 1999. It will stop being published at the beginning of 2022.

LIBOR, which has been active since 1986, has also met its doom. Partly due to BMR but mostly due to the mistrust following the scandal which resulted in the underlying market it measures no longer being liquid, U.K. regulators have decided that LIBOR will finish at the end of 2021.

The creation and adoption of new, risk-free, and BMR compliant benchmarks has already begun.

This is not the first time that a major shift has taken place in the benchmark sector. In the late 80’s and early 90’s, there was a transition from risk-free reference rates that were based on U.S. Treasury Bill rates towards riskier IBOR benchmarks based on euro/dollar rates.

What are the characteristics of these new benchmarks?

The new benchmarks that are set to substitute the old ones have a lower credit risk, are less volatile, harder to manipulate, and are in line with the IOSCO principles. They are more robust as they are anchored in active and liquid underlying markets.

They share two or more of the following characteristics:

1

They are based on overnight markets where volumes are larger.

2

They move beyond interbank markets to borrow from non-bank wholesale counterparties (investments funds, insurance companies, etc.)

3

In certain jurisdictions they draw on secured transactions rather than unsecured.

What are the new benchmarks?

The following benchmarks are in the process of substituting the old ones:

€STR – the Euro Short-Term Rate. First published on October 2, 2019 by the European Central Bank, it will substitute Eonia after it discontinues and will serve as a fallback rate for contracts referencing Euribor. It will be calculated on actual individual borrowing transactions in euro that are reported by banks in accordance with the ECB’s money market statistical reporting (MMSR). There are 50 MMSR banks compared to 28 banks on Eonia’s panel.

SONIA – the Sterling Over Night Index Average. It will substitute the Sterling LIBOR after it discontinues. It originally launched in 1997 but underwent several reforms in 2018 under the administration of the Bank of England. It’s measured on interest rates paid on a variety of eligible sterling denominated deposit transactions.

SARON – the Swiss Average Rate Overnight. It will substitute the Swiss Franc LIBOR after it discontinues. It is measured on transactions and quotes posted in the Swiss repo market. Repo markets, or repurchase agreement markets, are liquid, highly regulated, and stable and serve as the backbone of central bank activity and the financial industry.

SOFR – the Secured Overnight Financing Rate. It began its publication in April of 2018 after the U.S. Federal Reserve Bank's Alternative Reference Rates Committee selected it as an alternative to LIBOR. It’s based on the Treasury repo market.

An important group in Europe is the Working Group on Euro Risk-Free Rates. Set up by the European Central Bank (ECB), the Financial Services and Markets Authority (FSMA), the European Securities and Markets Authority (ESMA) and the European Commission, its task is to identify and recommend alternative euro risk-free rates and to work on an adoption plan to ensure a smooth transition to these alternative rates by all market participants.

What are some future problems for new benchmarks?

While BMR and the new risk-free benchmarks will have a positive impact on the benchmark sector, the transition will result in several problems that can’t be ignored.

SONIA and SARON are already up and running but their trading is so meagre that institutions are reluctant to switch. This means that liquidity remains low, making the two benchmarks seem uninviting, and thus creating a vicious circle.

There is also the issue of the migration of LIBOR-linked exposures towards the new benchmarks as trillions of dollars of legacy contracts will remain outstanding when LIBOR will be discontinued. To tackle this problem, it was suggested that contracts referencing IBOR rates run until 2050.

As BMR evolves and new benchmarks are born, it’s possible that several different benchmark formats will coexist, each with a purpose that fulfils different market needs.

E-commerce has revolutionized the way we do business but has also been used for criminal purposes. Learn how how legisl...

ComplianceWed 29 March 2023

Experts in risk management and regulatory compliance

Pideeco is a consultancy firm providing legal services, business solutions, operational assistance and educational material for professionals in the financial industry.

We are based in Brussels and we specialize in regulatory risk compliance services covering the Eurozone.

Pideeco combines professional Regulatory knowledge and technical expertise to safeguard your business’ reputational and operational risk. Our unique customer-centric approach helps us build strategical and legitimate cost-efficient remedies.

Working with us means reaching out to complementary people, allowing for original thinking and innovative vision.

Overall Responsibility of the Administrator

Overall Responsibility of the Administrator Oversight of third parties

Oversight of third parties Conflicts of interest for Administrators

Conflicts of interest for Administrators Control framework for Administrators

Control framework for Administrators Internal oversight

Internal oversight Quality of the benchmark

Quality of the benchmark Accountability

Accountability IOSCO Principles

IOSCO Principles