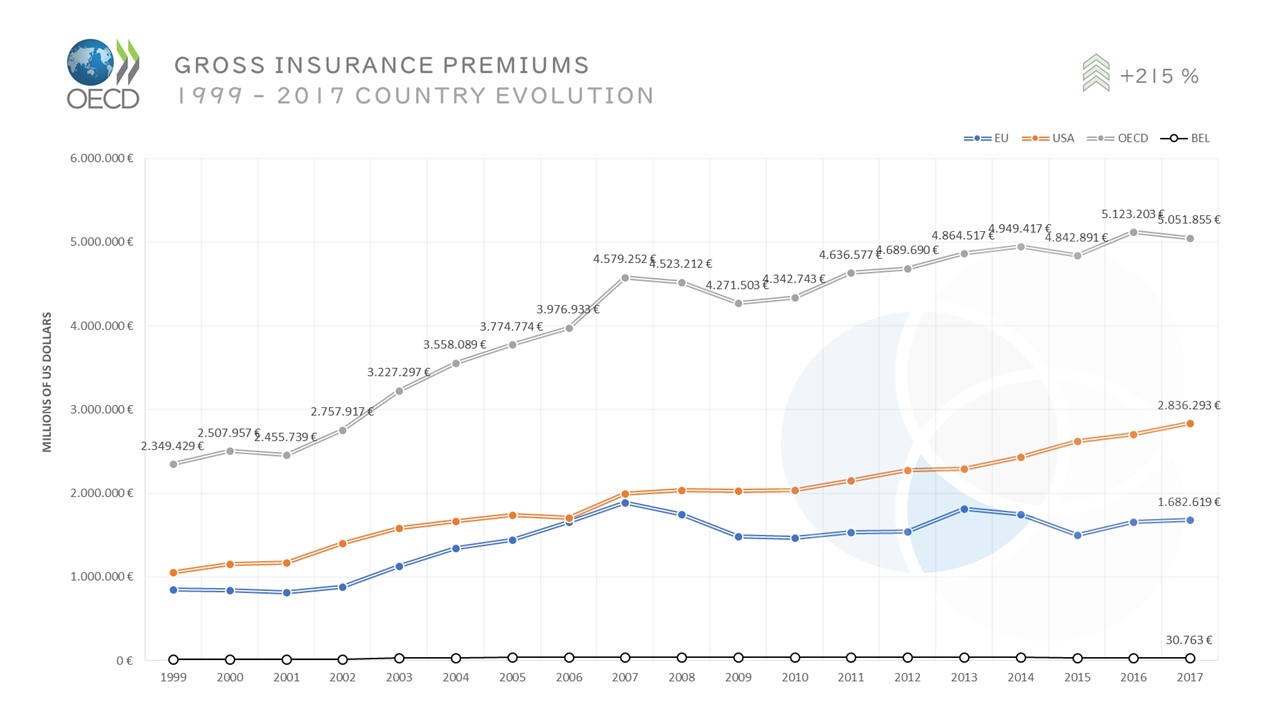

The Belgian government approved a bill according to which the insurance for legal protection will be tax deductible. This is expected to create a fiscal incentive for individuals and an augmentation of the premiums in the coming years.

Insurance is the transfer of the risk, from one entity/person to the insurance firm in exchange for premiums.

Reinsurance is an insurance acquired by an insurance firm in order to safeguard itself in case of a loss.

What is the scope of regulatory requirements for insurance firms?

The social-economic public interest characteristic of the insurance industry implies a strong regulatory framework, looking after the individuals as insurance consumers and policyholders.Financial solvency; Consumer protection; Transparency; Reporting; Governance; Ethics; Privacy are a few domains of recently expanding regulation to which insurance and reinsurance firms are entitled entities.

The Solvency II era and the Belgian implementation

Solvency II Directive (2009/138) introduced provisions for non-life insurance, life insurance and reinsurance companies and its aim is to promote transparency and competitiveness in the insurance sector. The Solvency II regime is following the regime of Basel II, which is applicable in the banking sector. Currently, Basel III applies. Basel standards and Solvency II apply to different sectors but both texts regulate -among others- issues on transparency, risks and capital.

In Belgium, the Law of 13 March 2016 on the legal status and supervision of insurance or reinsurance companies (the Solvency II Law) was transposed from the EU Directive. In addition, Circulars and Communications of the National Bank of Belgium (NBB) cover certain areas of the applicable legal requirements.

Two documents to consider are:

- Circular 2016/31 (updated in May 2020) on governance. Under this Circular the entities should have a proper governance system that reassures the sound management of the firm. The Circular provides guidance about the organisational structure of the entities, the independency of control functions, the policies (i.e. continuity policy), the reporting to the government.The update added a Standard form for the opinion of the person responsible for the compliance function on the outsourcing of a critical or important activity or function and a standard for notifying the NBB of a critical or important outsourcing.

- Circular 2012/14 on compliance function. The Circular provides rules for compliance professionals and their duties. The Compliance function must reassure that the entity works under honesty and integrity, following ethical standards and the applicable legal framework.

The PRIIPs Regulation: the KID as protective measure for the investors

Another regulation applicable for insurance/reinsurance entities is PRIIPs Regulation (1286/2014). According to the EU Commission "PRIIPs cover a range of investment products which, taken together, make up a market in Europe worth up to €10 trillion."

With KIDs, the regulator is trying to safeguard retail individuals against placing money on insurance products that they do not completely understand. The investor has to be able to compare key features, risks, potential future performance and costs in order to make an informed decision.

In February 2019, the Joint Committee of the European Supervisory Authorities (ESA) published recommendations regarding KIDs. According to ESA, retail investors are provided with "inappropriate expectations" about the possible returns they may receive. Hence, they propose that in the KID there must be included a warning to ensure that individuals are completely aware of the figures presented to them.

ESA published its technical advice on the PRIIPS regulation. The advice will be used by the European Commission for creating a strategy for retail investments and to make the right modifications to the PRIIPs legal framework.

The PRIIPs rules will be mandatory for the fund sector, starting from January 2023. The European Fund and Asset Management Association (EFAMA) published the revised version of the PRIIPs KID Q&A. The document should offer support to European fund managers.

The NBB and Financial Services and Markets Authority (FSMA) are the two supervisory authorities for insurance and reinsurance in Belgium. Although other relevant authorities in the EU, like the FCA in United Kingdom, are more advanced, the Belgian authorities make a continuous effort. Both the NBB and the FSMA improve in the way they inform, specify details and practice aspects of the EU and national legal framework. Their webpages (NBB and FSMA) are becoming more informative and the future seems very prominent.