What is DLU and how has it evolved through the years?

DLU stands for "Déclaration Libératoire Unique", which is a Single Discharge Declaration. By introducing the DLU concept, the scope of the Belgian tax authority was to give a chance, to people with assets in foreign accounts, to declare their assets to the Belgian authorities and receive some benefits for declaring.

The declaration-regularisation is applicable for income, sums, transactions VAT and capital. The legislation refers both to individuals and entities.

See below how the DLU legislation evolved across the years:The declaration-regularisation is applicable for income, sums, transactions VAT and capital. The legislation refers both to individuals and entities.

Why introducing a DLU 4 for fiscal regularisation?

Although there were three successive versions of acts of fiscal declaration-regularisation , the regulator inserted a fourth one : DLU 4 or DLU Quater, to fill in the gaps left from the previous versions.

More precisely, the second DLU included provisions regarding non-prescribed capital; however, nothing was provided for prescribed capital.

More precisely, the second DLU included provisions regarding non-prescribed capital; however, nothing was provided for prescribed capital.

"Fiscally Prescribed" capital is defined in the Belgian Law of 21 July 2016 as the capital which cannot be captured by the tax authorities, at the time of a declaration-regularisation, because the time limits have expired (depending always from the case).

In 2013 the third DLU introduced the idea to regularise prescribed capital, but it was only in 2016 that the new DLU 4 was devoted to this provision. The DLU 4 introduces the obligation for the contributors to declare (prescribed and non-prescribed) capital to the Belgian tax authority. It establishes a permanent fiscal regularisation mechanism against the "spontaneous" system established so far. This means that the declarants cannot impulsively and whenever they wish, declare their accounts. Since 2016, it is the authority who invites the applicants to submit their declarations during a specific period.

In exchange for their "honesty", the contributors will be offered fiscal and penal immunity. The declaration-regularisation can be used as evidence in case of a court procedure for administrative or other public services purposes.

Article 11 of the Belgian Law of 21 July 2016 provides some exceptions, according to which regularisation is not possible. These are cases where the money comes from illicit activities related to money laundering, financing of terrorism, organised crime, illicit trafficking of drugs, exploitation of prostitution, corruption in public position, environmentally severe crimes and other cases listed in the law. The regulator wants to avoid the "legalisation" of money coming from serious crimes.

How to submit your DLU foreign account declaration ?

The declaration should be submitted through a specific declaration form which will include the following information: the name of the declarant and, where applicable, that of his representative, the amount of income, sum, VAT transactions, prescribed capital and the filing date of the return.

The declaration should be submitted through a specific declaration form which will include the following information: the name of the declarant and, where applicable, that of his representative, the amount of income, sum, VAT transactions, and prescribed capital and the filing date of the return. You can find templates of the declaration forms provided under the Federal Public Finance Service webpage.

Accompanying documents will be submitted in 6 months after the submission of the DLU at the latest. If something is generated after the declaration was submitted and it is not relevant to the amount in the declaration, it will not be part of the DLU and will not be raised as a point in the future (i.e. for administrative or judiciary purposes). In some cases, there may be necessary to include an explanation of the fraud schemes from where the money is coming from. A levy will have to be paid also in 15 days. The declaration is submitted to the Point of Contact-Regularisations ("PCR" in French) which is created by the Federal Public Finance Service. The point of contact transmits the information to the Processing Unit. A FAQ DLU Quater (in French) was published by the Belgian government to provide clarifications and guidance for the declaration process.

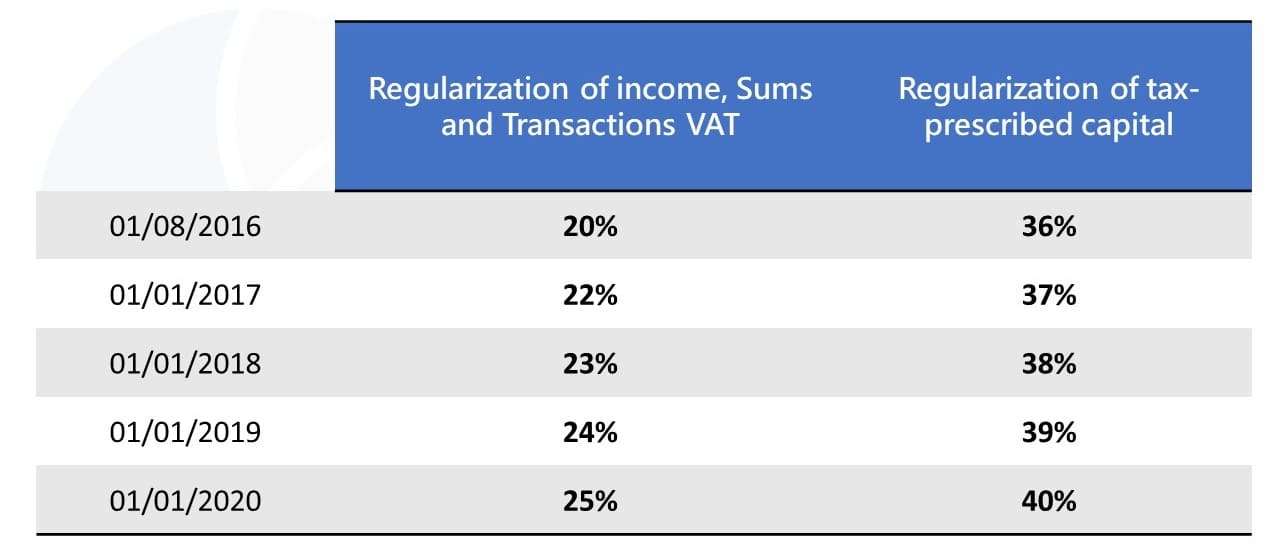

The individuals, after declaring income, sums, transactions VAT and capital, will have to pay the normal tax plus an additional 20-25% (the percentage changes every year, in 2020 it will be 25%). Tax prescribed income taxation is between 36-40% (the percentage changes every year) on the capital. The table below shows how tax percentages increased progressively :

Is fiscal and penal immunity enough to prompt Belgians to declare their foreign assets?

Regularising is the best way to avoid the risk of facing a trial. Has this advantage prompted more Belgians to declare their foreign accounts? The price of regularisation is heavy as taxation is becoming higher over the years. However, it is a solution for someone who wants to repatriate its capital to Belgium and take advantage of immunity.

Declarants should keep in mind that the DLU is not possible if they have been informed before submitting the declaration that an investigation will start against them by a Belgian judicial, tax administration, social security institution or a social inspection service or the Federal Public Finance Service.

What does the future bring for fiscal regularisation?

Do we expect the Belgian Tax authority to introduce a fifth DLU (DLU 5), in an effort to optimise the declaration-regularisation process in order to attract more declarants and as a result more money?Many taxpayers where hoping for more favourable treatment in the future. The people at stake will be more tempted from a less expensive regime. The "regularisation" taxation increased until 2020. The Belgian Monitor published a law on 16 March 2021, that would remove the permanent system of fiscal and social regularisation. The Act foresees that "Chapters 2 and 3 of the Act of 21 July 2016, to establish a permanent system of fiscal and social regularisation, shall cease to be in effect on 31 December 2023".

Requiring Assistance ?

Our professionals can support you and provide solutions to your case. Our experts are ready to provide you with more information regarding how you can conduct your declaration and prepare everything for you.

Thank you for this summary of DLU application!