Each year we are entitled to different lists about tax havens issued by governments or international organisations, but what is the difference between these lists?

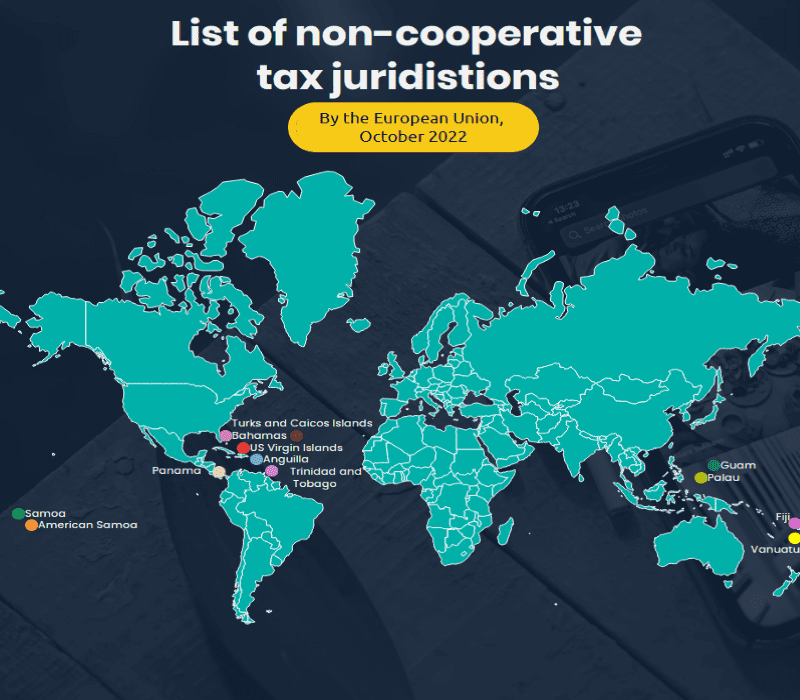

In October 2022, the European Union updated its list of non-cooperative tax jurisdictions :

When comparing the issued list to the financial secrecy index report of the Tax Justice Network (TJN) of 2022, one can notice that some European countries are present (Germany, Luxemburg, Netherlands in the top 20).

The Organisation for Economic Co-operation and Development (OECD) and others also share their lists each year.

As a company/financial institution, you should keep an eye on these lists to limit suspicious contacts with clients having accounts in those countries considered as dubious is essential to manage your risk exposure.

The Organisation for Economic Co-operation and Development (OECD) and others also share their lists each year.

As a company/financial institution, you should keep an eye on these lists to limit suspicious contacts with clients having accounts in those countries considered as dubious is essential to manage your risk exposure.

What is a tax haven country and how do they operate ?

There is no real standard legal definition, but the following elements can help us to gain a better comprehension about tax havens :Low taxation : This criterion only makes sense when one compares the tax rate of other countries with higher taxes in certain areas/activities. For example, this low taxation could impact only one category of taxpayer and for one category of their income. Therefore, a country may not be systematically regarded as a tax haven for all of its tax rules.

Confidentiality and lack of transparency : Confidentiality in relation to financial transactions and lack of transparency of the tax practices.

Each list of the different organisations is based on specific criteria. It should be clear enough to eliminate as much misunderstanding as possible.

Also, for some, there is not a single list but different lists with different levels. For instance, the European Union has two types of lists : the blacklist which includes countries that have not taken the necessary commitments (refusing to co-operate with European Union) and the greylist with countries that have made commitments to change their tax practices or legislation in the coming months.

Also, for some, there is not a single list but different lists with different levels. For instance, the European Union has two types of lists : the blacklist which includes countries that have not taken the necessary commitments (refusing to co-operate with European Union) and the greylist with countries that have made commitments to change their tax practices or legislation in the coming months.

How to avoid being a blacklisted country by the OECD ?

According to OECD ranking standards, to avoid being blacklisted, countries must demonstrate that they meet at least two of the three criteria established by the Global Forum on Transparency and Exchange of Information for Tax Purposes :- Compliance with the rules of information exchange on demand.

- The commitment to apply the standards of automatic information exchange.

- Be part of a multilateral mutual assistance convention or exchange network large enough to allow on-demand or automatic exchanges.

The most accurate and complete ranking would be the one of the Tax Justice Network. We find a ranking focused on financial opacity, taking into consideration more criterion than just the fact that a country has the lowest tax rate (automatic data exchange or not, existence of a register of the beneficiaries of the companies or not, size of the financial sector, banking secrecy impact, ...).

What does it really mean to be classified as a Tax Haven jurisdiction?

Generally, we put everyone in the same boat when we talk about tax havens, but the reality is that every situation is different and should be described carefully.

For instance, there is a difference between why Switzerland and Panama are considered tax havens.

The exercise implies to take a step back and look into the issue more closely. Such a vast difference brings discredit to certain classifications. Besides, the media does not go into detail and often reports confusing stories.

For instance, there is a difference between why Switzerland and Panama are considered tax havens.

The exercise implies to take a step back and look into the issue more closely. Such a vast difference brings discredit to certain classifications. Besides, the media does not go into detail and often reports confusing stories.

To understand the "tax haven" characteristics of a country, it is necessary to build knowledge on the topic and to go beyond the ethical and moral aspect. Public opinion must understand that a state could be considered as a tax haven for a specific tax regime impacting a determined type of taxpayer and even for a specific type of his/her income, and not for the whole tax regime applicable in this country. For example, it could be considered as such for non-taxation of dividends or royalties received abroad from a subsidiary of a group. For another State, it could be for its low taxation on income for companies. Another country for the rulings that the State gives more easily. Even Belgium has been grouped together with those tax haven countries for notional interest regime.

What are the real dangers associated with Tax Haven Countries ?

The main concern with tax havens is that most of them harbour an unquantifiable amount of assets intended for or generated by the laundering of money resulting from corruption, drug trafficking or even terrorism and other criminal activities.

That is the danger hidden behind the lack of transparency in those countries. Tax havens are not systematically used for illegal reasons, but in terms of transactions, the risk of confusing what is legal and what isn't, has extremely increased. As a reminder, within the EU zone, tax evasion through tax fraud is assimilated in "criminal activities", such as the ones described in the Fourth Anti-Money Laundering Directive.

What about the economic sanctions lists ?

The EU financial market actors are entitled to take extreme coercive measures including withdrawing financial institution licenses for proven lack of transparency or controls on business transactions occurring with certain countries. The European Commission has recently sued countries like Ireland for failing to recover 13 billion euros in back taxes from Apple; or Amazon, which, thanks to the tax advantages granted by Luxembourg, has largely escaped the corporate tax in Europe. A leaked list like in recent scandals (Panama Papers, LuxLeaks) makes more noise than an effective sharing of information.

While there are few sanctions to date, companies must consider the incurred risks (for example, the reputation impact on the company, or from a financial point of view the cost of non-transparency compliance created by the high amounts of the sanctions at stake as mentioned above.

Moreover, reputation is a highly important impact criterion: a transparent business will project a better picture of itself from which it will benefit directly in its activities, and above all will contribute to the transparency and stability of the global financial system.

Putting efficient and robust control processes based on the risk-based approach and effectively executing them avoids all these inconveniences. As the regulatory requirements will not decrease, we must strategically take the lead before laws and mandatory procedures are introduced.

Some countries were put under pressure and have made extensive efforts to be compliant as was revealed with the case of Switzerland that develops growing tax cooperation with Western countries. But concerning emerging countries, the matter is different as we develop towards double standards. We find ourselves in the concept that the Tax Justice Network nicknamed zebra: "clean, white money, for rich and powerful countries; dirty, black money for vulnerable and developing countries ".

Like in the US, we fight firmly against tax havens abroad, but we remain very lax at home like in Delaware... There are more and more pressures and efforts to harmonise and bring transparency. It's time to get in line to avoid high-risk exposures.

Tax Haven definition and recent European conclusions

In conclusion, the label "tax haven" has no official definition from a legal point of view. Each country has the right to decide its level of taxation. The situation lies in the financial shortfall for the countries because of the large-scale tax abuses and a lack of legal harmonisation between countries from the same economic zone, which could lead to the use of these non-transparent regimes to launder and use dirty money generated from terrorism, drugs trafficking and other illegal activities.Just think of the HSBC case and the accusation of complicity in money laundering for the benefit of traffickers and terrorists or the assistance offered to its clients for tax evasion, which profoundly impacted its reputation, but also obliged the bank to pay a record fine after their confession of their inability to effectively comply with regulations.

Financial SanctionsOECDFinancial firmsKYCComplianceTax HavensRed FlagsAMLRisk Based ApproachEUCorruptionKnow your Customer